How Many Properties Can You Identify in a 1031 Exchange? Understanding the 3-Property Rule in a 1031 Exchange.

- Marium Tariq

- Apr 22

- 14 min read

You are under contract on your investment property. Your Qualified Intermediary is in place. And now comes the question that trips up more investors than any other part of the identification process: how many replacement properties can you actually identify, and what rules govern that number?

The answer is not as simple as "three." The IRS gives investors three distinct frameworks for identifying replacement properties in a 1031 exchange, and the 3 property rule is just the most commonly used one. Each framework carries different limits, different acquisition requirements, and different consequences if you miscalculate. Choosing the wrong one for your situation, or accidentally violating its value threshold, can void an otherwise valid exchange.

This guide covers all three identification rules in plain language: how each one works, when each one makes strategic sense, and the specific mistakes that cause investors to lose their tax deferral at the identification stage. You will also find a side-by-side comparison and direct guidance from our experts at Above & Below 1031 on which rule fits which investor situation.

Quick answer: Under the three-property rule in a 1031 exchange, you can identify up to three replacement properties of any combined value and must acquire at least one. Under the 200% rule, you can identify more than three properties as long as their total fair market value does not exceed 200% of the relinquished property's sale price. The 95% exception allows the identification of more than three properties, but requires you to acquire at least 95% of the total identified value. All three rules are established under Treasury Regulation 1.1031(k)-1(c)(4) and only one may be used per exchange.

Table of Contents

Why the IRS limits how many properties you can identify

The three-property rule: the most commonly used option

The 200% rule: when three properties are not enough

The 95% exception: the rule you almost never see used

Side-by-side comparison: which rule fits your situation

Common mistakes investors make with identification rules

Frequently asked questions

Why does the IRS limit how many properties you can identify?

Before 1991, investors in deferred 1031 exchanges could identify unlimited replacement properties with no restrictions on quantity or value. Predictably, some investors listed dozens of properties as a hedge with no genuine commitment to acquiring any of them.

The IRS moved to close that loophole. The identification rules were codified through the 1991 Treasury Regulations, which established the three-property rule, 200% rule, and 95% exception as the governing framework for all deferred exchanges.

The practical consequence of that history: the IRS treats identification rule violations as failures of intent, not paperwork errors. If an exchanger fails to comply with one of the three identification options, the exchange is disallowed in its entirety. No partial credit. No course correction after Day 45.

The rules are mutually exclusive

This single detail causes more identification errors than any other. The three rules are not a tiered system you move through automatically. A taxpayer must adhere to one of the three identification rules, and the rules are mutually exclusive — only one may be used per exchange.

What does that mean in practice? If you identify three properties under the three-property rule and then add a fourth to your notice, you have not shifted to the 200% rule. You have created a notice that potentially violates both rules simultaneously. This is one of the most common identification errors, and it is entirely avoidable with early planning before the clock starts.

What counts as an identified property?

The identification count is not limited to your written notice. Two categories of property count toward your total:

Written identification submitted to your QI before midnight of Day 45

Properties closed within the 45-day window: these are automatically deemed identified under IRS rules, even without a formal written notice, unless additional properties will be purchased after day 45. A property purchased before Day 45 still counts toward the three-property and 200% rule limits and must be listed on your identification form if you intend to acquire additional properties.

Practical example: an investor closes on a replacement property on Day 30, then submits a written identification for two more properties on Day 44. All three slots under the three-property rule are now used, even though one has already been purchased.

For an even more detailed account of the 45-day identification rule in 1031 exchanges, read here.

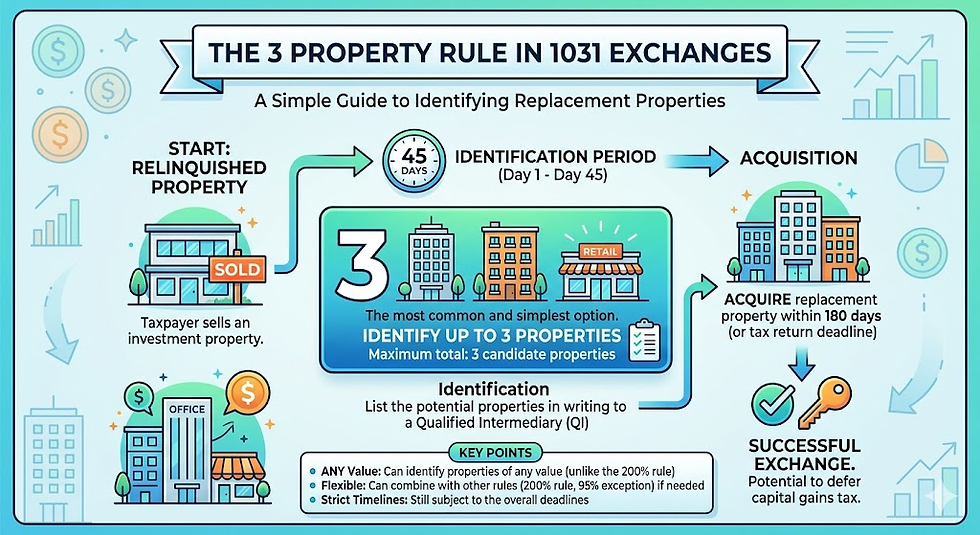

The 3-property rule in 1031 exchanges is the most commonly used option

The three-property rule is the default identification framework for the vast majority of 1031 exchange investors, and for good reason. It is the most straightforward, carries the lowest risk of a technical error, and gives investors meaningful flexibility without complex value calculations.

What the rule allows

The three-property rule allows investors to identify up to three potential replacement properties of any combined value and to acquire one, two, or all three of the identified properties, as long as the total value of what is acquired meets or exceeds the value of the relinquished property to fully defer capital gains taxes.

The key phrase is "any combined value." Unlike the 200% rule, the three-property rule places no ceiling on aggregate fair market value. You can sell a $400,000 rental and identify three properties each worth $2 million. The values are irrelevant. Only the count matters.

How it works in practice

An investor sells a duplex for $600,000 and identifies three replacement properties:

A single-family rental at $650,000

A small commercial building at $800,000

A Delaware Statutory Trust interest at $400,000

They only need to close on one to complete the exchange. If their first-choice property falls through on Day 60, they still have two valid options remaining on their list. The combined value of $1,850,000 would exceed the 200% rule threshold, but under the three-property rule, that is irrelevant.

The strategic case for using all three slots

Most investors understand they can identify three properties. Fewer treat all three slots as a strategic tool rather than an optional provision.

Here is why:

Deals fall through during inspection, financing, and title review, often after Day 45, when no substitutions are possible

Having two backup options does not require you to close on them; it simply keeps your exchange alive if your primary choice fails

Using a Delaware Statutory Trust or other passive investment as Property 3 gives you a fast-closing safety net that can often close within days if your first two options collapse

The three-property rule is the most commonly used identification option specifically because it allows investors to identify fallback properties in the event their preferred replacement property cannot be acquired. That protection only exists if you actually use the slots.

The one misconception to address

You are not required to acquire all three identified properties. You are not required to acquire them in any particular order. The only acquisition requirement under the three-property rule is that you close on at least one identified property and that the total value of what you acquire equals or exceeds the relinquished property's sale price for a fully tax-deferred exchange.

The 200% rule in a 1031 exchange: when three properties are not enough

When an investor's strategy requires identifying more than three replacement properties to provide more options or because they want to acquire more than three properties, the 200% rule provides that flexibility. The 200% rule allows investors to identify any number of replacement properties, provided that the total fair market value of all identified properties does not exceed 200% of the sale price of the relinquished property.

Unlike the three-property rule, which ignores value entirely, the 200% rule makes aggregate fair market value the controlling factor. Get the math wrong and the identification is invalid.

How to calculate the 200% limit

The calculation is straightforward:

Step 1: Determine the sale price of your relinquished property.

Step 2: Multiply by two. That is your 200% ceiling.

Step 3: Add up the fair market values of every property on your identification list. The total must stay below the ceiling.

A concrete example: an investor sells a rental property for $800,000. Their 200% limit is $1,600,000. They identify five replacement properties with a combined fair market value of $1,500,000 (within the limit), so the identification is valid, and they can acquire any combination of those five properties within the 180-day exchange period.

If they add a sixth property that pushes the total to $1,700,000, the identification is potentially invalid. The entire exchange is at risk unless the 95% exception can be satisfied, which carries its own significant requirements.

Note: like the three-property rule, the 200% rule does not require the investor to acquire all identified properties. They only need to close on enough to meet the equal-or-greater-value requirement for full tax deferral. The 200% limit governs identification only, not acquisition.

The DST leverage trap under the 200% rule

When identifying a Delaware Statutory Trust as a replacement property, the IRS looks at the number of properties held in each DST offering for property count and the value of the exact percentage of ownership that the investor would potentially be acquiring when considering the value for ID'ing purposes.

Investors must account for both equity and debt when calculating the total value of replacement properties under the 200% rule, which is especially important when investing in leveraged DSTs.

An investor splitting proceeds across multiple DSTs alongside one or two direct properties can easily push past the 200% ceiling without realizing it, simply by miscounting the leveraged values. We flag this as one of the most common calculation errors seen, and it is one that a QI who actively reviews identification notices before submission will catch before it voids the exchange.

When the 200% rule makes strategic sense

The 200% rule is the right framework in three specific situations:

Portfolio repositioning. An investor selling one large property and diversifying proceeds into four or five smaller assets across different markets or asset classes. The three-property rule's three-slot limit is simply too restrictive for this strategy.

DST diversification. An investor splitting exchange proceeds across multiple passive DST investments, each held by a different sponsor or in a different asset class, where more than three interests need to be identified.

Preserving additional options. An investor who has already committed all three slots under the three-property rule and recognizes they need additional backups. Switching to the 200% rule before the identification notice is submitted, not after, keeps that option available within the value ceiling.

Pro Tip! It is important to keep a record of the FMV of each property at the time of identification as proof of values in the event of an audit in the future.

The 95% exception: the 1031 identification rule you almost never want to rely on

The 95% exception allows investors to identify any number of replacement properties with no limit on total value, but requires them to acquire at least 95% of the total fair market value of all identified properties by the end of the 180-day exchange period.

On paper, this sounds like maximum flexibility. In practice, it is the most restrictive of the three frameworks because the acquisition requirement is nearly impossible to satisfy if anything goes wrong.

Why this rule is almost never used

The math leaves no room for error. Consider this scenario: an investor identifies ten properties with a combined fair market value of $3,000,000. To satisfy the 95% exception, they must acquire at least $2,850,000 worth of those properties within 180 days.

If one deal falls through: one seller backs out, one property fails inspection, one lender delays. The investor may fall below the 95% threshold and lose their entire identification. The whole exchange is disqualified, not just the property that failed.

As a practical matter, the 95% exception is difficult to adhere to and is rarely used. In the real world, investors who rely on it almost always end up buying everything on their identification list, which is essentially the only way to guarantee compliance.

Compared to the three-property rule, which requires closing on just one property, and the 200% rule, which requires no specific acquisition percentage, the 95% exception offers the least forgiveness of any identification framework.

Which 1031 exchange identification rule fits your situation? A side-by-side comparison

Before choosing an identification rule, it helps to see all three side by side. The table below covers the five dimensions that matter most to investors deciding how to structure their identification notice.

Three-property rule | 200% rule | 95% exception | |

Maximum properties | 3 | Unlimited | Unlimited |

Value limit | None | 200% of sale price | None |

Acquisition required | At least 1 | At least 1 | At least 95% of total value |

Best use case | Single replacement with backups | Portfolio diversification or DSTs | Single-seller portfolio acquisition |

Risk level | Low | Moderate | High |

The right rule depends entirely on what you are trying to accomplish with the exchange. Here are example scenarios for when each rule may be beneficial.

Situation 1: Selling one rental property and buying one replacement with two backups. Use the three-property rule. Identify your first-choice property and one or two back up properties. This gives you additional property options without risking the value limit restrictions of the other two rules.

Situation 2: Selling one large property and diversifying into four or five smaller assets or DSTs. Use the 200% rule, with careful value calculation before submitting the notice. Add up the full fair market values of every identified property — including leveraged DST values — and confirm the total stays below 200% of your sales price. Do this early in the identification period, not on day 44 when time to correct any errors may be limited.

Situation 3: Acquiring an entire portfolio from a single seller. The 95% exception may apply, but only with experienced QI oversight and high certainty that you will close on 95% or more of the total identified value. If any single acquisition in the portfolio falls through and drops you below the 95% threshold, the entire exchange is at risk. This scenario warrants a direct consultation before the identification period opens.

Common mistakes investors make with 1031 exchange identification rules

Most identification errors are preventable. The five mistakes below appear regularly enough at Above & Below 1031 that we address each one at the start of every client engagement.

Mistake 1: Using the 200% rule without accounting for DST leverage. Investors identify several DSTs alongside direct properties, add up only their equity contributions, and assume they are within the 200% ceiling. The IRS counts the full property investment value including debt. A $200,000 equity stake in a 50%-leveraged DST counts as $400,000 toward the aggregate limit. This single error could void exchanges that are otherwise structured correctly.

Mistake 2: Identifying only one property under the three-property rule. Even when an investor is already certain which replacement property they want, they should consider ID'ing one or two additional properties. If the primary deal falls through on Day 60, with no backups listed, there is nothing left to close on. The exchange fails and the proceeds become fully taxable. Identifying a second or third replacement property could save an exchange.

Mistake 3: Treating the rules as a tiered system. An investor identifies three properties, then adds a fourth to the notice, assuming they have automatically shifted to the 200% rule. They have not. The three identification rules are mutually exclusive, and a taxpayer may only use one rule at a time per exchange. Adding a fourth property to a three-property notice creates a potential violation of both rules simultaneously if the aggregate value exceeds 200% of the sale price.

Mistake 4: Submitting identification revisions after Day 45. Investors sometimes believe they can update their identification list once they have more information about a property's condition or value. Revisions are only valid within the 45-day identification window. The exchanger may change the properties identified as often as they want during the 45-day identification period, but the identification must be delivered by midnight of the 45th day. After that, the list is locked permanently.

Mistake 5: Forgetting that early closings count toward the identification limit. An investor closes on a replacement property on Day 20 of the identification period and then submits a written identification for three additional properties on Day 40 — believing they have three slots remaining. They do not. A property purchased prior to the 45th day counts toward the three-property and 200% rule limits. The early closing consumed one slot, leaving only two available for the written notice.

Frequently asked questions about the 3-property identification rules 1031 exchange

Do you have to buy all the properties you identify in a 1031 exchange?

No. Under both the three-property rule and the 200% rule, you only need to acquire at least one identified property — not all of them. The only exception is the 95% rule, which requires you to acquire properties totaling at least 95% of the aggregate fair market value of everything on your identification list. For most investors using the three-property rule, closing on one property of equal or greater value to the relinquished property is sufficient for a fully tax-deferred exchange.

Can you identify more than three properties in a 1031 exchange?

Yes, but not under the three-property rule. If a taxpayer identifies more than three properties, they move to the 200% rule, which requires the aggregate fair market value of all identified properties to not exceed 200% of the sale price of the relinquished property. If the 200% threshold is exceeded, the 95% exception applies, requiring the investor to acquire at least 95% of the total identified value. Only one of the three rules may be used per exchange.

What happens if you violate the 200% rule in a 1031 exchange?

Violating the 200% rule means the identification notice is invalid unless the 95% exception requirements can be satisfied. If a taxpayer's list contains more than three properties and is not in compliance with the 200% rule, the taxpayer will not be eligible for tax deferral under Section 1031 unless they are able to satisfy the 95% exception. If neither rule is satisfied, the exchange is disqualified entirely and the proceeds from the relinquished property become fully taxable in the year of sale.

Can you change your identified properties after Day 45?

No. The identification window closes at midnight on Day 45, and no changes, additions, or substitutions are permitted after that point. The taxpayer can revoke a property from their identification list and add new ones as many times as needed during the 45-day period, but the final list must be submitted before the window closes. If a property on your list becomes unavailable after Day 45, your only options are the remaining identified properties. This is why identifying genuine backup options before the deadline matters so much.

What is the difference between the three-property rule and the 200% rule in a 1031 exchange?

The three-property rule limits the number of identified properties to three but places no ceiling on their combined value. The 200% rule removes the three-property limit but caps the aggregate fair market value of all identified properties at 200% of the relinquished property's sale price. According to the IRS guidelines on like-kind exchanges, both rules are established under Treasury Regulation 1.1031(k)-1(c)(4) and serve the same underlying purpose: ensuring investors make a genuine, committed identification rather than listing unlimited options as a hedge.

Can you identify a Delaware Statutory Trust as a replacement property in a 1031 exchange?

Yes. A DST interest qualifies as like-kind replacement property in a 1031 exchange. When using the 200% rule and identifying a DST, the full fair market value of the underlying property — including any leveraged debt — counts toward the 200% aggregate limit, not just the investor's equity contribution. Investors identifying multiple DSTs alongside direct properties should calculate their total identified value using the gross property values before submitting their identification notice. The number of properties held in each DST offering also counts towards the number of properties identified.

Do identified replacement properties have to be under contract?

No. The IRS does not require identified properties to be under contract, in escrow, or actively listed at the time of identification. The identification simply requires an unambiguous written description, typically a street address or legal description, signed by the exchanger and delivered to the Qualified Intermediary before midnight of Day 45. A property can be identified based on its complete address alone, even if no formal purchase agreement exists yet.

What happens if one of my identified properties falls through before Day 180?

If a property on your identification list becomes unavailable after Day 45, you must close on one of your other identified properties to complete the exchange. No substitutions or additions to the list are permitted after the identification window closes. This is the core reason why ID'ing one or two back up properties can save an exchange.

3-property rule in a 1031 exchange: Work with Above & Below 1031 on your identification strategy

Choosing the wrong identification rule when submitting an ID letter is not a recoverable mistake after Day 45. Once the 45-day clock starts, the rule you follow, the properties you list, and the values you calculate are locked in. Getting those decisions right from the beginning can protect everything that follows.

At Above & Below 1031, Whitney reviews every client's identification strategy during the identification window, not after Day 45. That conversation covers which rule fits your investment goals, how to calculate your value ceiling if you are using the 200% rule, how to account for DST leverage in your totals, and how to structure your backup options just in case they're needed.

Contact Above & Below 1031 before your property closes. That one conversation is the difference between an identification strategy that protects your exchange and one that puts it at risk.

Disclaimer: This article is intended for educational purposes only and does not constitute legal, tax, or financial advice. Every 1031 exchange involves unique facts and circumstances. Consult a qualified tax advisor or attorney before initiating an exchange or making identification decisions.

About the Author

Whitney Nash, CES® is the founder of Above & Below 1031 LLC, a Qualified Intermediary and Certified Exchange Specialist. She works with real estate investors across Texas and nationwide, guiding first-time exchangers, accidental landlords, and portfolio investors through every stage of the 1031 exchange process — from pre-sale planning through final closing on replacement property. Above & Below 1031 is based in McKinney, Texas.

Comments